Quick Answer

To pay off multiple debts without feeling overwhelmed, list every debt in one place, keep making minimum payments on all accounts where possible, choose a clear repayment strategy such as debt snowball or debt avalanche, focus extra money on one debt at a time, and review your progress monthly. Turning several debts into one structured plan makes repayment easier to understand and far easier to stick with.

The aim is not to solve everything in one day. The aim is to remove confusion, choose a direction, and make your next payment part of a bigger plan.

Why Multiple Debts Feel So Overwhelming

Multiple debts feel difficult because they create mental clutter. One balance might be on a credit card, another on a personal loan, another on a store card, and another on car finance. Each one has its own payment date, interest rate, minimum payment, and statement. Even if the total amount is manageable over time, the number of moving parts can make it feel much harder than it really is.

The emotional side matters too. When you owe money in several places, it is easy to feel pulled in different directions. You may wonder which payment matters most, whether you should spread extra money across everything, or whether you are falling behind even when you are making payments. That uncertainty creates anxiety, and anxiety often leads to avoidance.

The real problem is not always the number of debts. It is the lack of a clear system. Once every debt is organised and given a role in the plan, the situation usually feels less chaotic.

The Biggest Mistake People Make

The biggest mistake people make with multiple debts is trying to tackle everything at once. It sounds sensible at first. If you owe money in several places, it feels natural to send a little extra to each debt and hope that everything gradually improves.

The problem is that this approach often spreads your effort too thinly. You make payments, but no single debt seems to move much. Because progress is hard to see, motivation drops. Then the plan starts to feel pointless, even though you are genuinely trying.

A stronger approach is to keep every account stable with minimum payments where possible, then focus extra money on one target debt. This gives your repayment plan a clear direction and makes progress easier to recognise.

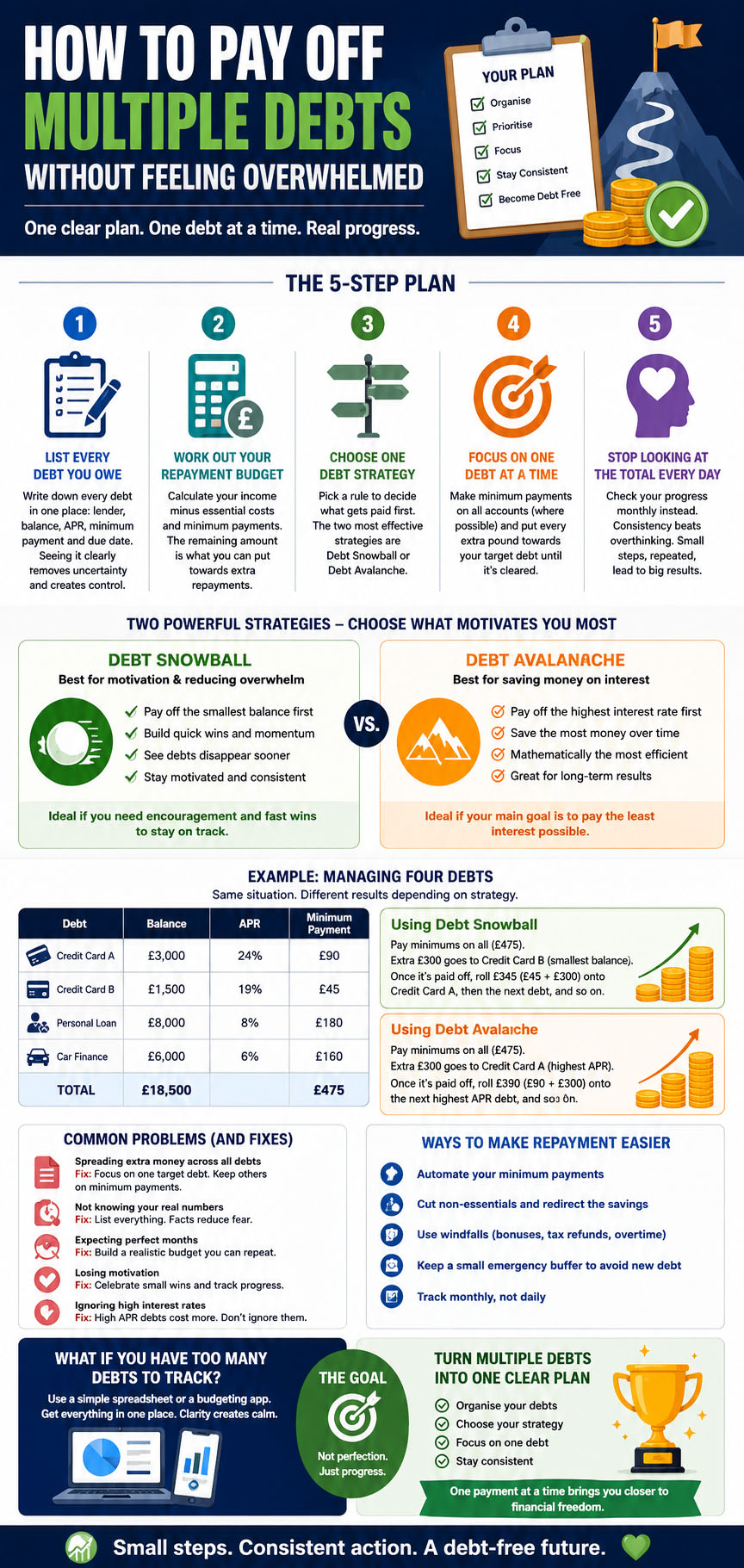

Step 1: List Every Debt You Owe

Before you can pay off multiple debts properly, you need to see them clearly. This is the step many people avoid, but it is also the step that usually creates the first real feeling of control.

Write down every debt in one place. Include the lender or account name, current balance, interest rate or APR, minimum monthly payment, and payment due date. If you are not sure of the details, check your latest statements or online accounts.

| Debt | Balance | APR | Minimum Payment |

|---|---|---|---|

| Credit Card A | £3,000 | 24% | £90 |

| Credit Card B | £1,500 | 19% | £45 |

| Personal Loan | £8,000 | 8% | £180 |

| Car Finance | £6,000 | 6% | £160 |

Seeing the full picture might feel uncomfortable at first, but it removes uncertainty. Once the debts are visible, they become easier to manage. You are no longer relying on memory, worry, or guesswork.

Step 2: Work Out Your Total Debt Repayment Budget

After listing your debts, the next question is simple: how much can you realistically put towards debt each month?

Start with your income, then subtract essential living costs such as housing, utilities, food, transport, insurance, and other necessary expenses. Then account for your minimum debt payments. What remains is the amount you may be able to use for extra repayments, savings buffer, or other priorities.

This is where many people go wrong. They set a repayment amount that looks impressive but does not fit real life. A plan that requires perfect conditions every month is fragile. One car repair, higher food bill, or unexpected cost can knock it off course.

A sustainable repayment budget is better than an extreme one. Debt repayment is not about one heroic month. It is about building a rhythm you can repeat.

Step 3: Choose One Debt Strategy

When you have several debts, you need a rule for deciding what gets paid first. Without a rule, you may end up making emotional decisions, reacting to whichever debt feels most annoying that week.

Two of the most common repayment strategies are the debt snowball method and the debt avalanche method. Both can work well, but they solve slightly different problems.

Debt snowball

The debt snowball method focuses on the smallest balance first, regardless of interest rate. You make minimum payments on everything else, then put extra money towards the smallest debt. Once that debt is cleared, you roll its payment into the next smallest debt.

Snowball is often helpful for people who feel overwhelmed because it creates quick wins. Clearing a small debt can give you proof that the plan is working, which makes it easier to keep going.

Debt avalanche

The debt avalanche method focuses on the highest interest rate first. You still make minimum payments on the other debts, but your extra money goes towards the debt costing you the most in interest.

Avalanche is usually the strongest method mathematically because it can reduce the total interest paid. The trade-off is that your first win may take longer if the highest interest debt also has a large balance.

The best strategy is not always the one that sounds cleverest. It is the one you can actually follow. If you need motivation, snowball may feel easier. If you are focused on saving the most interest, avalanche may suit you better.

Step 4: Focus on One Debt at a Time

Once you choose a strategy, the next part becomes simpler. You keep every account moving with minimum payments where possible, then direct extra money towards one target debt.

This single-target focus is powerful because it reduces decision fatigue. You do not need to keep asking where the extra money should go. The plan already tells you.

It also makes progress more visible. If you put an extra £150 towards one debt, you can see that balance falling faster. If you split that same £150 across five debts, the impact may feel almost invisible.

Multiple debts become less overwhelming when only one debt is the main focus at any given time.

Step 5: Stop Looking at the Total Every Day

When you owe money across several accounts, the total debt figure can feel intimidating. Looking at it constantly may make repayment feel slower than it really is.

The total matters, of course, but it is not always the most helpful number to focus on day to day. Large debt totals tend to move gradually. If you check too often, you may feel disappointed even when things are improving.

Instead, focus on milestones. Your first milestone might be clearing the smallest debt. Another might be reducing your total by £1,000. Later, it might be reaching 25% repaid, 50% repaid, or getting below a major balance threshold.

Milestones make a long journey feel more manageable. They turn one big number into a series of smaller wins.

How Debt Snowball Reduces Overwhelm

The debt snowball method is popular for a reason. It works with human behaviour, not just maths. When you are overwhelmed, motivation matters. Seeing a debt disappear can change how you feel about the whole process.

Imagine you have four debts, and the smallest balance is £500. If you focus extra money on that one first, you may clear it quickly. Suddenly, four debts become three. That visible change can make the situation feel lighter.

The snowball method may not always save the most interest, but it can be extremely helpful if your main challenge is staying engaged. For many people, confidence is what keeps the plan alive.

How Debt Avalanche Reduces Total Interest

The debt avalanche method reduces overwhelm in a different way. Instead of giving you the quickest emotional win, it gives you confidence that your money is being used as efficiently as possible.

High interest debt is expensive. If one credit card has an APR of 29% and another loan has an APR of 8%, the credit card is likely costing you more for every pound owed. Paying the higher interest debt first can reduce the amount of interest that builds up over time.

Avalanche can feel slower at the beginning, especially if the first target debt is large, but it often produces stronger interest savings. It is well suited to people who are motivated by efficiency and long-term cost reduction.

A Real Example of Someone Managing Four Debts

Let’s say someone has four debts with a total balance of £15,000. They owe £2,500 on Credit Card A, £1,200 on Credit Card B, £7,000 on a personal loan, and £4,300 on car finance.

| Debt | Balance |

|---|---|

| Credit Card A | £2,500 |

| Credit Card B | £1,200 |

| Personal Loan | £7,000 |

| Car Finance | £4,300 |

Their minimum payments come to £450 per month, and they can afford an extra £250 per month. That gives them a total repayment budget of £700.

If they use the snowball method, they may focus on Credit Card B first because it has the smallest balance. Once that is cleared, the money previously going to that card can be added to the next debt. The repayment power grows over time.

If they use the avalanche method, they may start with the highest APR account instead. That may save more interest, but the first visible win could take longer. The right choice depends on what will keep them consistent.

Common Problems When Managing Multiple Debts

Multiple debts create several common problems. One is missed payment dates. Even when someone has enough money to pay, different due dates can cause confusion. Setting reminders or automating minimum payments can reduce that risk.

Another problem is forgetting the real balances. If you only have a rough idea of what you owe, it is hard to make good decisions. Updating your debt list monthly helps keep the plan accurate.

Emotional decision-making is another issue. Some people pay whichever debt is annoying them most, rather than the debt that fits the strategy. Others constantly switch between snowball and avalanche, which makes the plan feel unstable.

The solution is not perfection. It is consistency. Choose a system, follow it long enough to see results, and adjust only when there is a good reason.

Ways to Make Debt Repayment Feel Easier

Paying off multiple debts does not have to consume your whole life. In fact, the better organised your plan is, the less mental energy it should require.

Automating payments can help. At the very least, automating minimum payments reduces the risk of missed due dates. Reviewing progress monthly, rather than daily, can also make the process feel calmer.

It also helps to celebrate milestones. Clearing a debt, reducing your total by £1,000, or reaching the halfway point are all meaningful moments. They remind you that progress is happening, even if the full journey still has some distance to go.

Finally, expect imperfect months. A difficult month does not mean the plan has failed. It just means you review, adjust if needed, and continue.

What If You Have Too Many Debts to Track?

If you have several debts, trying to track everything manually can become frustrating. This is where a debt payoff calculator or planner can be genuinely useful.

A good tool can help you enter each debt, compare repayment strategies, see the effect of extra payments, and estimate your debt-free date. That removes a lot of guesswork.

Visual timelines can also help reduce overwhelm. Instead of seeing debt as a confusing group of balances, you can see a path. That path may still take effort, but it becomes easier to understand.

Turning Multiple Debts Into One Clear Plan

Multiple debts do not have to mean chaos. Most of the overwhelm comes from not knowing what to focus on first, not knowing how long repayment may take, and not being able to see how today’s payments connect to the bigger picture.

Once you list your debts, work out your repayment budget, choose a strategy, and focus on one target at a time, the situation becomes far easier to manage. You still have work to do, but you are no longer trying to fight every debt at once.

If you want to see exactly how your debts could be repaid, compare debt snowball and debt avalanche strategies, calculate your estimated debt-free date, and understand how extra payments affect your timeline, try the free PayOffPlan debt calculator.

There is no signup, no account required, and no email needed. Your debt information stays private on your own device. Open the app, enter your debts, and turn multiple balances into one clear repayment plan.