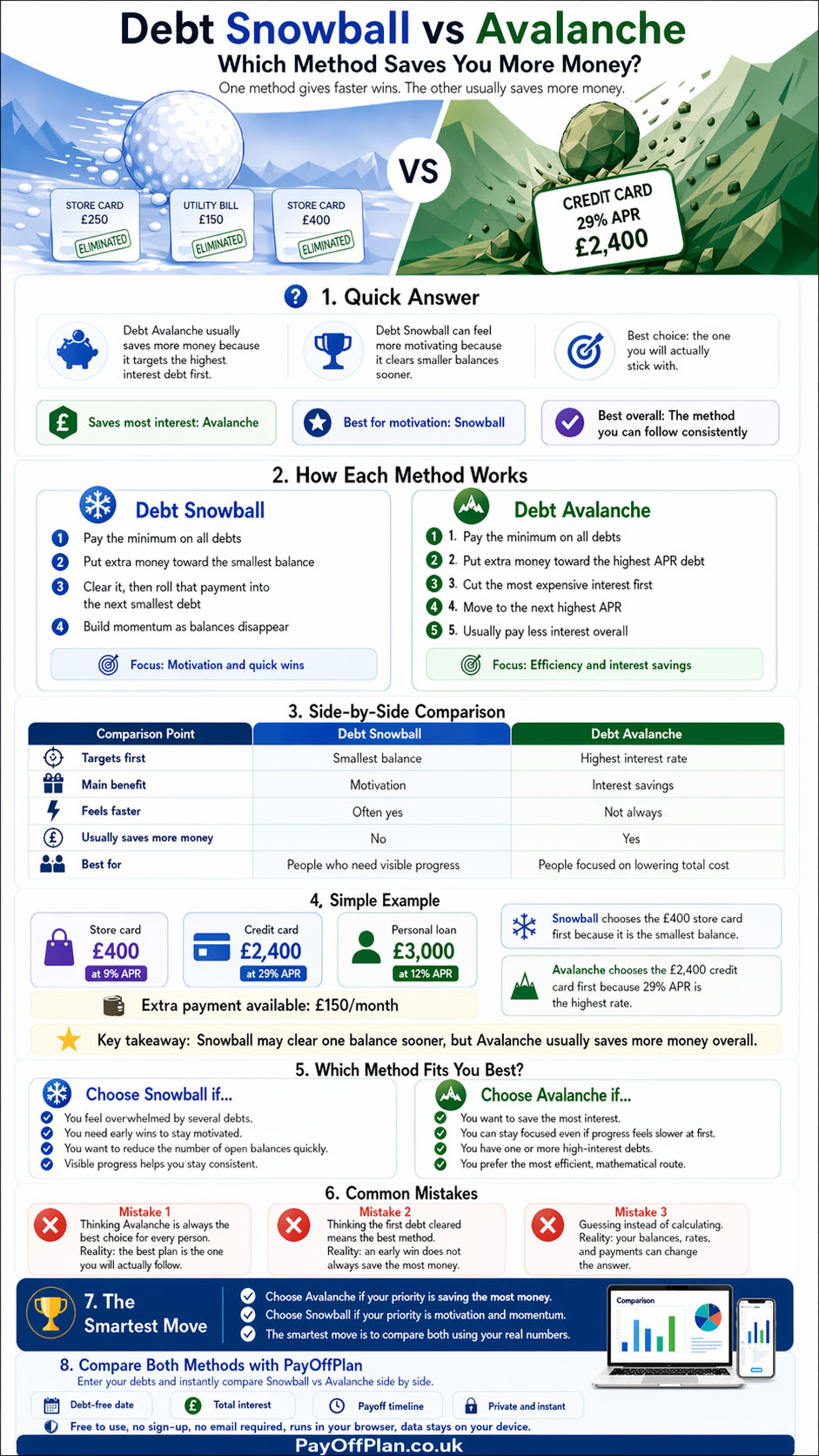

Quick answer: which method saves more money?

In most cases, the debt avalanche method saves more money than the debt snowball method. That is because avalanche targets the highest interest debt first, which reduces the amount of expensive interest building up over time. The snowball method focuses on the smallest balance first, which can feel more motivating but often costs more overall.

That said, the cheapest method on paper is not always the method someone follows best in real life. If the snowball method keeps you engaged and consistent, it can still be a very strong strategy. The real goal is not only to save money, but to finish the journey.

What is the debt snowball method?

The debt snowball method means paying the minimum payment on all your debts while putting any extra money towards the smallest balance first. Once that smallest debt is cleared, you roll the payment you were making on it into the next smallest balance. Over time, your payment power grows, which creates the “snowball” effect.

This method is popular because it gives you visible progress early. Clearing a small balance can happen relatively quickly, and that early success can feel like a genuine turning point. When someone has several debts hanging over them, even one balance disappearing can make the situation feel lighter and more manageable.

That emotional momentum is the main strength of the snowball method. It is designed to keep you moving, even if it is not usually the cheapest path in terms of total interest.

What is the debt avalanche method?

The debt avalanche method also starts with minimum payments across all debts, but instead of targeting the smallest balance first, it targets the highest interest rate first. Any extra money goes straight at the most expensive debt, while the rest continue to receive their minimum payments.

The logic is straightforward. High-interest debt costs you more every month it stays around. By reducing that first, you cut the total amount of interest charged across the life of your repayment plan. This is why the avalanche method is widely seen as the mathematically optimal option.

Its weakness is not financial, it is behavioural. If the highest interest debt also has a large balance, it may take longer before you get the satisfaction of fully clearing one account. For some people, that makes progress feel slower, even when they are saving more money overall.

Why the avalanche method usually saves more money

Interest is what makes debt drag on and cost more than expected. The longer a high-interest balance stays unpaid, the more money disappears into charges instead of actually reducing the principal. That is the heart of why the avalanche method usually comes out ahead.

Imagine two debts. One has a small balance but a low rate, and the other has a larger balance with a very high APR. If you attack the small one first because it is easier to clear, the high-interest debt keeps growing more expensive in the background. If you attack the highest APR first, you start reducing the costliest part of your debt stack immediately.

Over months and years, that difference adds up. In many real-world cases, avalanche does not just save a little money, it can save a meaningful amount of interest, especially if credit card rates are involved.

Why some people still choose the snowball method

If avalanche usually saves more money, why do so many people still choose snowball? Because money is only part of the equation. Human behaviour matters just as much.

Debt repayment is not a one-week project. It can take months or years. Along the way, motivation dips, unexpected costs appear, and people start questioning whether their effort is making any difference. The snowball method responds to that problem by creating earlier wins. You see balances disappear sooner, which can make the whole process feel more achievable.

For someone who needs visible momentum to stay committed, that psychological lift can be extremely valuable. A plan that is slightly less efficient financially but actually followed to completion can still beat a more efficient plan that loses your attention halfway through.

Debt snowball vs avalanche: the side-by-side comparison that matters

The easiest way to think about these methods is not in terms of which one is universally better, but in terms of what each one is designed to do.

The snowball method is built around momentum. It helps you clear debts faster in terms of the number of accounts disappearing, which can make the journey feel more rewarding. It often suits people who feel overwhelmed by having too many balances open at once.

The avalanche method is built around efficiency. It focuses on reducing your most expensive debt first, which usually lowers total interest and can make the overall cost of repayment smaller.

So the real comparison looks like this: snowball often wins on motivation and visible progress, while avalanche usually wins on interest savings and mathematical efficiency. The better method depends on which of those matters more in your situation.

A simple example: which method saves more money in practice?

Let’s use a simple example. Imagine you have three debts. The first is a store card with a balance of £400 at 9% APR. The second is a credit card with a balance of £2,400 at 29% APR. The third is a personal loan with a balance of £3,000 at 12% APR. You are making minimum payments on all three and can put an extra £150 per month towards one target debt.

Under the debt snowball method, you would attack the £400 store card first because it is the smallest balance. That would probably feel great when it disappears. After that, the freed-up payment would roll into the next smallest balance.

Under the debt avalanche method, you would target the credit card at 29% APR first, even though it is not the smallest balance. That means the most expensive debt gets reduced earlier, which slows the growth of interest charges.

In a case like this, the avalanche method would usually save more money overall because that 29% APR debt is far more expensive than the others. The snowball method could still clear one balance faster, but it would often allow the most costly debt to continue building interest for longer.

This is the key point. Snowball may feel faster, because you see a debt disappear sooner. Avalanche often is cheaper, because you stop feeding the most expensive balance first.

Does avalanche always win on cost?

In most normal repayment scenarios, yes, avalanche will usually come out ahead on total interest. That is exactly what it is built to do. But it is worth understanding the nuance.

If your debts all have very similar interest rates, the savings gap between snowball and avalanche may be quite small. In that kind of situation, the emotional boost of clearing smaller balances first could be more valuable than chasing a relatively minor difference in total cost.

So while avalanche is usually the money-saving winner, the degree of that advantage can vary. That is why it makes sense to compare your actual debts rather than relying only on general advice.

Which method gets you debt-free faster?

This is where people often get confused, because “saving more money” and “feeling faster” are not always the same thing. The avalanche method can sometimes help you become debt-free sooner overall, especially when high-interest debts are doing a lot of damage in the background. But that does not always mean it feels faster emotionally.

The snowball method often delivers the faster emotional win because one of your accounts disappears earlier. That can make the process feel like it is moving quickly, even if the total interest cost ends up being higher.

So if you are asking which method gets you debt-free faster, the honest answer is that avalanche often improves efficiency, while snowball often improves motivation. The actual timeline difference depends on your balances, interest rates, minimum payments, and any extra money you can add.

How to choose the right method for your personality and finances

The best debt strategy is the one you will realistically follow. That is the most important rule.

If you are disciplined, focused on reducing interest, and can stay consistent even if the first payoff takes a while, the avalanche method is often the strongest choice. It is designed to reduce the cost of debt as efficiently as possible.

If you know you need visible progress to stay motivated, or if you are feeling mentally overloaded by several open balances, the snowball method may suit you better. Clearing one debt early can make the whole plan feel more achievable.

Many people also start with one method and then switch later once they understand their own behaviour better. That is perfectly reasonable. What matters is not loyalty to a label, but finding a structure that helps you keep going.

What people often get wrong when comparing snowball and avalanche

One common mistake is assuming that because avalanche saves more money, it must always be the superior choice. In theory, it often is. In practice, behaviour matters. A plan only works if it gets used.

Another mistake is focusing only on which debt gets cleared first. That can be misleading. The first debt to disappear may make you feel better, but it does not necessarily tell you which method will cost less overall.

Some people also compare the methods without using real numbers. They guess which one will be better instead of calculating the likely debt-free date, total interest, and overall repayment order. That makes the decision far less useful than it could be.

The best comparison is not theoretical. It is personal. It shows how both strategies perform using your own balances, rates, and payment amounts.

The easiest way to compare both methods properly

If you want a proper answer to the snowball vs avalanche question, the easiest route is to compare both methods side by side using a calculator. That lets you see more than just a vague explanation. You can look at your debt-free date, the total interest paid under each strategy, the order your debts would be cleared, and how extra monthly payments change the outcome.

This matters because the same general advice can play out very differently depending on the debts involved. A person with one very high-interest credit card may see a large advantage from avalanche. Someone with similar rates across all debts may find the difference much smaller.

Once you can see both strategies clearly, the decision becomes far easier. You are no longer choosing based on theory alone. You are choosing based on your own numbers.

Compare snowball vs avalanche with PayOffPlan

If you want to know which method saves more money for your exact situation, PayOffPlan makes that comparison simple. You can enter your debts, add any extra monthly payment, and instantly compare the snowball and avalanche methods side by side.

You will be able to see your estimated debt-free date, the likely payoff timeline, and the difference in total interest paid. That means you do not need to rely on rough assumptions or mental maths. You can see which strategy looks better for your actual debts in minutes.

The tool is free to use, requires no sign-up, no account, and no email, and it runs in your browser. Your data stays on your device, so you can compare strategies privately and instantly.

The debt avalanche method usually saves more money. The debt snowball method may still be the better fit for some people because it supports consistency. The best way to know which one is right for you is to compare both properly and see the numbers for yourself.